|

REMITTANCES |

|

by Valentino Piana (2007) |

|

|

|

|||

|

Contents |

||

|

|

||

|

Money sent home from emigrants working abroad. A key financial flow directed (mainly) to developing countries, which helps financing consumption, savings, and investments, and improves the balance of payments. Remittances help fight poverty, in both urban and rural areas. In many countries, remittances are higher foreign direct investment and development assistance. More formally, in World Bank report GEP 2006, data on international migrants' remittances are measured in U.S. dollars as the sum of three components recorded in the Balance of Payment: workers' remittances, compensation of employees, and migrant tranfers.

The total amount of remittances is positively linked to: 1. the number of emigrants abroad; 2. the income of emigrants, which, in turn, is higher when: 2.1. the countries in which they are concentrated are rich; 2.2. their jobs are remunerated with high wages, which requires a favourable legal setting, a non-discriminatory labour market, a rising level of personal and social competences; 2.3. a high level of employment of emigrants; 3. the savings that emigrants can afford, balancing income with living expenditure; 4. the willingness to send money home, influenced by emotional links (e.g. family) as well as by rational perspectives (e.g. coming back). Many host countries, however, maintain quotas for new immigrants, discriminate against foreigners, have large share of illegal immigration, exploited by employers, which pay extremely low wages. Job segregations is frequent as well, with certain nationalities being accepted in certain jobs but not in others. The high cost of sending and receiving money limits the effectiveness of remittances. But competition among banks and money transfer agencies can reduce fees, to the effect that more of the hard earned money sent by migrant workers goes to the people who depend on it. Money transfer fees are the lowest in those countries where there is greater competition. Remittance sending patterns vary across gender in many countries: in some cases, males send more than female migrants while in other countries it is the reverse. Much depends on gender job segregation and the proportion of the kind of reasons that lead to the migration. Migrants with wide family linkages send more than those who are getting disconnected from the network. At micro-level, the bulk of remittances is mainly used in their current consumption which are often in poverty. Anthropological and migration research, as well as household surveys, indicate strongly the importance of this flow as part of an income stream for remittance receiving households. Remittances contribute to improved standards of living, better health and education, human and financial asset formation (land, livestock, in building or improving a home). Studies show that most remittances are used for: * Daily needs and expenses, (consumption

improving the recipients' standard of living); The number of people living out of remittances from relatives and friends can be narrow or large depending on social networks. At territorial level, a key open issue is how to convert remittances into a financial boost for development. At macro-level, if large, remittances can boost the balance of payments, sometimes sustaining trade deficits and the appreciation of exchange rate. The consumption part of remittances trigger the Keynesian multiplier, boosting GDP and employment, to the extent it is directed towards goods and services produced within the country. A part might be leaking towards imports. Remittances used to purchase houses might provoke a general rise in the price per square metre of housing, which can lead to a housing bubble (with speculative purchases in view of selling at higher prices). There is thus the risk that the families that do not receive remittances are crowded out by the families that do (mirroring a sort of "empoverishing growth"). Remittances could finance entrepreneurial activities as seed money and business loans, leading to new firms and investments, if adequate institutional settings were in place, as the Economics Web Institute proposes to channel remittances to microfinance. Remittances

are steadily growing worldwide. Their growth is gradual and widely distributed.

The largest receivers of remittances are India, China, Mexico, and Philippines.

The main host countries from which remittances are sent are the United

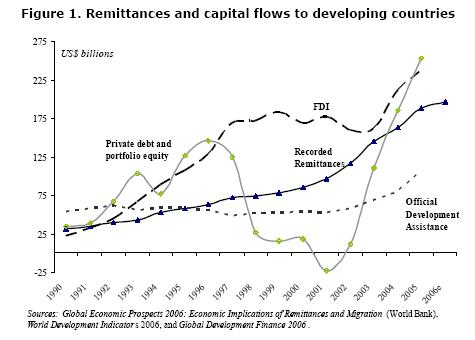

States of America, Germany, France, and Canada. As emigrants are spreading geographically, the number of host countries is widening, which stabilizes the flows, potentially also during the business cycle. A comparison with other financial flows, as FDI, is given in this graph:

Source: Briefing by World Bank (Nov. 2006) There is growing use of new technologies and new channels of remittance transmission, as through mobile phones (in this respect, the Philippines are a relevant case study). Behaviour during the business cycle The business cycle in receiving countries usually does not influence the remittances flows. Also in case of devaluation, which would possibly reduce trust in the country, remittances remain stable in international currency as dollars or euros because they are gained abroad. The structural elements (demographics, social integration, emancipation, etc.) are more important than host country cycle, although if the foreign minority is large and concentrated in poorly paid jobs, recession might hit them severely, with a corresponding fall in remittances. Several policies have been called for, in order to reduce the cost of sending remittances (which constitute a sort of double taxation), to monitor these flows (to avoid they fund illegal organizations), to complement remittances to obtain the largest societal effects. In particular, our Economics Web Institute has been devising,

push and experimenting a policy to connect remittances to microfinance

institions. To know more, feel free to contact

us. The bilateral matrix of remittances (212 countries x 212 countries) and its methodology Outflows and inflows of remittances: a time series Emigrants

stock in 220 countries by nationality and place of birth Presentation

of a new policy channelling remittances to microfinance 2006 Global Economic Prospects (GEP) by World Bank Remittances in the Philippines: a pro-local development approach Filipino diaspora, remittances, and poverty The effects on family linkages of Filipino emigration and remittances How the migrant domestic workers live

|

||